McConnell Campbell R., Brue Stanley L., Barbiero Thomas P. Microeconomics. Ninth Edition

Подождите немного. Документ загружается.

terms and concepts

210 Part Two • Microeconomics of Product Markets

variable costs vary with output. The total cost

of any output is the sum of fixed and variable

costs at that output.

7. Average fixed costs, average variable costs,

and average total costs are fixed, variable,

and total costs per unit of output. Average

fixed cost declines continuously as output

increases because a fixed sum is being

spread over an increasing number of units of

production. A graph of average variable cost

is U-shaped, reflecting the law of diminish-

ing returns. Average total cost is the sum of

average fixed and average variable costs; its

graph is also U-shaped.

8. Marginal cost is the extra, or additional, cost

of producing one more unit of output. It is the

amount by which total cost and total variable

cost change when one more or one fewer

unit of output is produced. Graphically, the

marginal-cost curve intersects the ATC and

AVC curves at their minimum points.

9. Lower resource prices shift cost curves

downward, as does technological progress.

Higher input prices shift cost curves upward.

10. The long run is a period of time sufficiently

long for a firm to vary the amounts of all

resources used, including plant size. In the

long run all costs are variable. The long-run

ATC, or planning, curve is composed of seg-

ments of the short-run ATC curves, and it

represents the various plant sizes a firm can

construct in the long run.

11. The long-run ATC curve is generally U-

shaped. Economies of scale are first en-

countered as a small firm expands. Greater

specialization in the use of labour and man-

agement, the ability to use the most efficient

equipment, and the spreading of startup

costs among more units of output all con-

tribute to economies of scale. As the firm

continues to grow, it will encounter dis-

economies of scale stemming from the

managerial complexities that accompany

large-scale production. The output ranges

over which economies and diseconomies

of scale occur in an industry are often an

important determinant of the structure of

that industry.

plant, p. 181

firm, p. 181

industry, p. 181

sole proprietorship, p. 181

partnership, p. 181

corporation, p. 181

stocks, p. 183

bonds, p. 183

limited liability, p. 183

double taxation, p. 183

principle–agent problem,

p. 183

economic (opportunity) cost,

p. 184

explicit costs, p. 185

implicit costs, p. 185

normal profit, p. 185

economic profit, p. 186

short run, p. 187

long run, p. 187

total product (TP), p. 188

marginal product (MP), p. 188

average product (AP), p. 188

law of diminishing returns,

p. 188

fixed costs, p. 192

variable costs, p. 192

total cost, p. 192

average fixed cost (AFC),

p. 194

average variable cost (AVC),

p. 194

average total cost (ATC),

p. 195

marginal cost (MC), p. 195

economies of scale, p. 202

diseconomies of scale, p. 203

constant returns to scale,

p. 203

minimum efficient scale

(MES), p. 207

natural monopoly, p. 207

study questions

1. Distinguish between a plant, a firm, and an

industry. Why is an industry often difficult to

define?

2.

KEY QUESTION What are the major

legal forms of business organization? Briefly

state the advantages and disadvantages of

each. How do you account for the dominant

role of corporations in the Canadian economy?

3. “The legal form an enterprise takes is dic-

tated primarily by the financial requirements

of its particular line of production.” Do you

agree? Why or why not?

4.

KEY QUESTION Gomez runs a small

pottery firm. He hires one helper at $12,000

per year, pays annual rent of $5000 for his

shop, and spends $20,000 per year on

chapter eight • the organization and the costs of production 211

materials. He has $40,000 of his own funds

invested in equipment (pottery wheels, kilns,

and so forth) that could earn him $4000 per

year if alternatively invested. He has been

offered $15,000 per year to work as a pot-

ter for a competitor. He estimates his en-

trepreneurial talents are worth $3000 per

year. Total annual revenue from pottery

sales is $72,000. Calculate the accounting

profit and the economic profit for Gomez’s

pottery firm.

5. Which of the following are short-run and

which are long-run adjustments? (a) Wendy’s

builds a new restaurant. (b) Acme Steel Cor-

poration hires 200 more workers. (c) A

farmer increases the amount of fertilizer

used on his corn crop. (d) An Alcan alu-

minum plant adds a third shift of workers.

6.

KEY QUESTION Complete the fol-

lowing table by calculating marginal product

and average product from the data given.

Inputs of Total Marginal Average

lalbour product product product

00

1 15 ______ ______

2 34 ______ ______

3 51 ______ ______

4 65 ______ ______

5 74 ______ ______

6 80 ______ ______

7 83 ______ ______

8 82 ______ ______

Plot the total, marginal, and average prod-

ucts and explain in detail the relationship

between each pair of curves. Explain why

marginal product first rises, then declines,

and ultimately becomes negative. What

bearing does the law of diminishing returns

have on short-run costs? Be specific. “When

marginal product is rising, marginal cost is

falling. When marginal product is diminish-

ing, marginal cost is rising.” Illustrate and

explain graphically.

7. Why can the distinction between fixed costs

and variable costs be made in the short run?

Classify the following as fixed or variable

costs: advertising expenditures, fuel, interest

on company-issued bonds, shipping charges,

payments for raw materials, real estate taxes,

executive salaries, insurance premiums, wage

payments, depreciation and obsolescence

charges, sales taxes, and rental payments

on leased office machinery. “There are no

fixed costs in the long run; all costs are vari-

able.” Explain.

8. List several fixed and variable costs associ-

ated with owning and operating an automo-

bile. Suppose you are considering whether

to drive you car or fly 1000 kilometres for

spring break. Which costs—fixed, variable,

or both—would you take into account in

making your decision? Would any implicit

costs be relevant? Explain.

9.

KEY QUESTION A firm has $60 in

fixed costs and variable costs as indicated in

the table below. Complete the table; check

your calculations by referring to question 4

at the end of Chapter 9.

Total Total Average Average Average

Total fixed variable Total fixed variable total Marginal

product cost cost cost cost cost cost cost

0 $______ $ 0 $______ $______ $______ $______ $______

1 ______ 45 ______ ______ ______ ______ ______

2 ______ 85 ______ ______ ______ ______ ______

3 ______ 120 ______ ______ ______ ______ ______

4 ______ 150 ______ ______ ______ ______ ______

5 ______ 185 ______ ______ ______ ______ ______

6 ______ 225 ______ ______ ______ ______ ______

7 ______ 270 ______ ______ ______ ______ ______

8 ______ 325 ______ ______ ______ ______ ______

9 ______ 390 ______ ______ ______ ______ ______

10 ______ 465 ______ ______ ______ ______ ______

212 Part Two • Microeconomics of Product Markets

a. Graph total fixed cost, total variable cost,

and total cost. Explain how the law of

diminishing returns influences the shapes

of the variable-cost and total-cost curves.

b. Graph AFC, AVC, ATC, and MC. Explain

the derivation and shape of each of these

four curves and their relationships to one

another. Specifically, explain in nontech-

nical terms why the MC curve intersects

both the AVC and ATC curves at their

minimum points.

c. Explain how the location of each curve

graphed in question 7b would be altered

if (1) total fixed cost had been $100 rather

than $60, and (2) total variable cost had

been $10 less at each level of output.

10. Indicate how each of the following would

shift the (1) marginal-cost curve, (2) average-

variable-cost curve, (3) average-fixed-cost

curve, and (4) average-total-cost curve of a

manufacturing firm. In each case specify the

direction of the shift.

a. A reduction in business property taxes

b. An increase in the nominal wages of pro-

duction workers

c. A decrease in the price of electricity

d. An increase in insurance rates on plant

and equipment

e. An increase in transportation costs

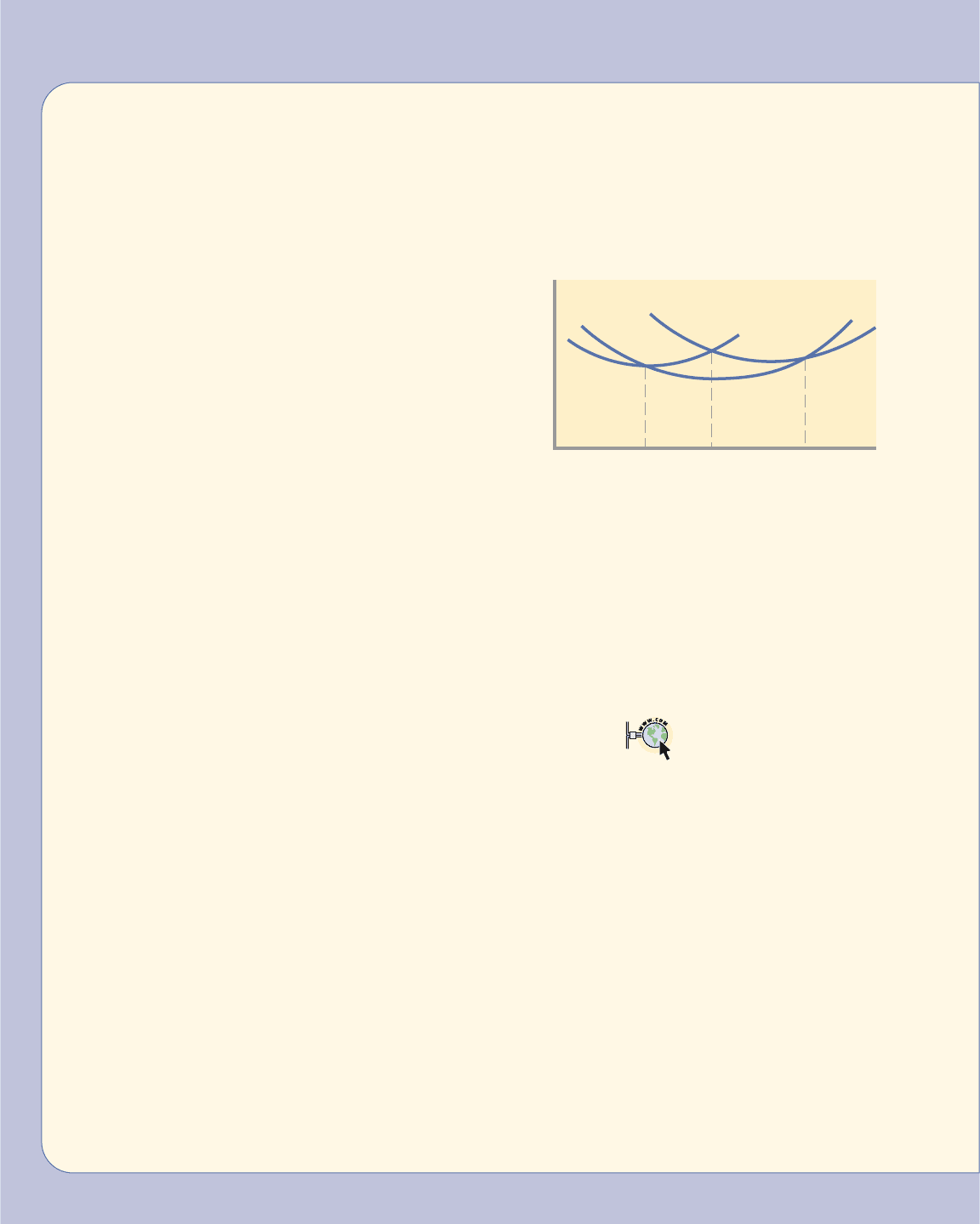

11. Suppose a firm has only three possible

plant-size options, represented by the ATC

curves shown in the accompanying figure.

What plant size will the firm choose in pro-

ducing (a) 50, (b) 130, (c) 160 and (d) 250

units of output? Draw the firm’s long-run

average-cost curve on the diagram and

describe this curve.

12.

KEY QUESTION Use the concepts of

economies and diseconomies of scale to

explain the shape of a firm’s long-run ATC

curve. What is the concept of minimum effi-

cient scale? What bearing can the shape of

the long-run ATC curve have on the structure

of an industry?

13. (The Last Word) What is a sunk cost? Provide

an example of a sunk cost other than one

from the text. Why are such costs irrelevant

in making decisions about future actions?

internet application questions

1. Check out the National Post 500 list of

the largest Canadian firms at <www.

nationalpostbusiness.com/datamining/top500/

top500.htm>. From the top ten profit list, select

three firms from three different industries

and discuss the likely sources of economies

of scale that underlie their large size.

2. Use the Yahoo search engine at <www.

yahoo.ca> to locate a company’s homepage

of your choice. Find and review the com-

pany’s income statement in its annual report

and classify the nonrevenue items as either

fixed or variable costs. Are all costs clearly

identifiable as either fixed or variable? What

item would be considered as accounting

profit? Would economic profit be higher or

lower than this accounting profit?

ATC

ATC

3

ATC

2

ATC

1

0

80 150 240

Q

IN THIS CHAPTER

IN THIS CHAPTER

Y

Y

OU WILL LEARN:

OU WILL LEARN:

The four basic market

structures and how they

determine the degree of

competition among firms.

•

The four conditions required for

perfectly competitive markets.

•

The profit-maximizing output

in the short-run for a firm

in pure competition.

•

About the marginal cost and

the short-run supply curve.

•

About the firm’s profit

maximization in the long run.

•

That in competitive markets

firms attain both allocative and

productive efficiency.

Pure

Competition

I

n Chapter 7 we examined the relationship

between product demand and total rev-

enue, and in Chapter 8 we discussed costs

of production. Now we want to put revenues

and costs together to see how a business

decides what price to charge and how much

output to produce. A firm’s decisions con-

cerning price and production depend greatly

on the character of the industry in which it

is operating; there is no average or typical

industry. At one extreme is a single producer

that dominates the market; at the other

extreme are industries in which thousands of

firms each produce a minute fraction of mar-

ket supply. Between these extremes are many

other industries.

NINE

Since we cannot examine each industry individually, we will focus on several basic

models of market structure to help you understand how price and output are deter-

mined in the many product markets in the economy. The models will also help you

to assess the efficiency or inefficiency of those markets.

Economists group industries into four distinct market structures: pure competi-

tion, pure monopoly, monopolistic competition, and oligopoly. These four market

models differ in several respects: the number of firms in the industry, whether

those firms produce a standardized product or try to differentiate their products

from those of other firms, and how easy or how difficult it is for firms to enter the

industry.

Very briefly the four models are as follows:

● Pure competition is a market structure that requires a very large number of

firms producing a standardized product (that is, a product identical to that of

other producers, such as corn or cucumbers). New firms can enter the indus-

try very easily.

● Pure monopoly is a market structure in which one firm is the sole seller of a

product or service (for example, a local cable company). Since the entry of

additional firms is blocked, one firm constitutes the entire industry. Because

the monopolist produces a unique product, it makes no effort to differentiate

its product.

● Monopolistic competition is characterized by a relatively large number of

sellers producing differentiated products (clothing, furniture, books). There is

widespread nonprice competition, a selling strategy in which one firm tries to

distinguish its product or service from all competing products based on attrib-

utes like design and quality (an approach called product differentiation). Entry

to monopolistically competitive industries is quite easy.

● Oligopoly involves only a few sellers of an identical or similar product; con-

sequently each firm is affected by the decisions of its rivals and must take those

decisions into account when determining its own price and output.

Table 9-1 summarizes the characteristics of the four models for easy comparison. In

discussing these four market models, we will occasionally distinguish the charac-

teristics of a pure competition from those of the three other basic market structures,

which together we will designate as imperfect competition.

Let’s take a fuller look at pure competition, the focus of the remainder of this chapter.

● Very large numbers A basic feature of a purely competitive market is the pres-

ence of a large number of sellers acting independently, often offering their

products in large national or international markets. Examples include markets

for farm commodities, the stock market, and the foreign exchange market.

214 Part Two • Microeconomics of Product Markets

Pure Competition: Characteristics

and Occurrence

Four Market Models

pure

competition

A market structure

in which a very large

number of firms

produce a standard-

ized product.

pure

monopoly

A

market structure in

which one firm is

the sole seller of a

product or service.

monopolistic

competition

A market structure

in which a relatively

large number of

sellers produce

differentiated

products.

oligopoly A

market structure in

which a few large

firms produce homo-

geneous or differen-

tiated products.

imperfect

competition

The market models

of pure monopoly,

monopolistic com-

petition, and oligop-

oly considered as

a group.

● Standardized product Purely competitive firms produce a standardized (or

homogeneous) product. As long as the price is the same, consumers will be

indifferent about which seller to buy the product from. Buyers view the prod-

ucts of firms B, C, D, and E as perfect substitutes for the product of firm A.

Because purely competitive firms sell standardized products, they make no

attempt to differentiate their products and do not engage in other forms of

nonprice competition.

● Price-takers In purely competitive markets individual firms exert no signif-

icant control over product price. Each firm produces such a small fraction of

total output that increasing or decreasing its output will not perceptively

influence total supply or, therefore, product price. In short, the competitive

firm is a price-taker: it cannot change market price, it can only adjust to it. That

means that the individual competitive producer is at the mercy of the market.

Asking a price higher than the market price would be futile; consumers will

not buy from firm A at $2.05 when its 9999 competitors are selling an identical

product at $2 per unit. Conversely, because firm A can sell as much as it

chooses at $2 per unit, it has no reason to charge a lower price, say, $1.95, for

to do so would lower its profit.

● Free entry and exit New firms can freely enter, and existing firms can freely

leave, purely competitive industries. No significant legal, technological, finan-

cial, or other obstacles prohibit new firms from selling their output in any com-

petitive market.

chapter nine • pure competition 215

TABLE 9-1 CHARACTERISTICS OF THE FOUR BASIC

MARKET MODELS

MARKET MODEL

Monopolistic

Characteristic Pure competition competition Oligopoly Pure monopoly

Number of firms A very large Many Few One

number

Type of product Standardized Differentiated Standardized or Unique; no close

differentiated substitutes

Control over price None Some, but within Limited by mutual Considerable

rather narrow interdependence;

limits considerable with

collusion

Conditions of Very easy, no Relatively easy Significant Blocked

entry obstacles obstacles

Nonprice None Considerable Typically a great Mostly public

competition emphasis on deal, particularly relations

advertising, brand with product advertising

names, trademarks differentiation

Examples Agriculture Retail trade, Steel, automobiles, Local utilities

dresses, shoes farm implements,

many household

appliances

price-taker

A firm in a purely

competitive market

that cannot change

market price, only

adjust to it.

Relevance of Pure Competition

Although pure competition is relatively rare in the real world, this market model is

highly relevant. A few industries more closely approximate pure competition than

any other market structure. In particular, we can learn much about markets for agri-

cultural goods, fish products, foreign exchange, basic metals, and stock shares by

studying the pure competition model. Also, pure competition is a meaningful start-

ing point for any discussion of price and output determination. The operation of a

purely competitive economy provides a standard, or norm, for evaluating the effi-

ciency of the real-world economy.

To develop a tabular and graphical model of pure competition, we first examine

demand from a competitive seller’s viewpoint and see how it affects revenue. This

seller might be a wheat farmer, a strawberry grower, or a sheep rancher. Each purely

competitive firm offers only a negligible fraction of total market supply, therefore, it

must accept the price determined by the market; it is a price-taker, not a price-maker.

Perfectly Elastic Demand

The demand curve of the competitive firm, as represented by columns 1 and 2 in

Table 9-2, is perfectly elastic. As shown in the table, the market price is $131. The

firm represented cannot obtain a higher price by

restricting its output, nor does it need to lower

its price to increase its sales volume.

We are not saying that market demand is per-

fectly elastic in a competitive market. Market

demand graphs are the usual downsloping

curve, as a glance ahead at Figure 9-7(b) will

reveal. In fact, the total-demand curves for most

agricultural products are quite inelastic, even

though agriculture is the most competitive

industry in the Canadian economy. An entire

industry (all firms producing a particular

product) can affect price by changing industry

output. For example, all firms, acting inde-

pendently but simultaneously, can increase

price by reducing output, but the individual

firm cannot do that. So the demand schedule

faced by the individual firm in a purely compet-

itive industry is perfectly elastic at the market

price, as shown in Figure 9-1.

Average, Total, and Marginal Revenue

The firm’s demand schedule is also its revenue

schedule. The price per unit to the purchaser is

also revenue per unit, or average revenue, to

the seller. To say that all buyers must pay $131

per unit is to say that the revenue per unit, or

average revenue, received by the seller is $131.

216 Part Two • Microeconomics of Product Markets

<n103dept.matc.edu/

walshj/chrono/

Chrono%202/

purecomp3.htm>

A quick summary of

pure competition

Demand for a Purely Competitive Seller

TABLE 9-2 THE DEMAND

AND REVENUE

SCHEDULES

FOR A PURELY

COMPETITIVE FIRM

FIRM’S DEMAND FIRM’S

SCHEDULE REVENUE DATA

(1) (2) (3) (4)

Product Quantity Total Marginal

price, P demanded, revenue, revenue,

(average Q TR MR

revenue) (1) × (2)

$131 0 $ 0

131 1 131

$131

131 2 262

131

131 3 393

131

131 4 524

131

131 5 655

131

131 6 786

131

131 7 917

131

131 8 1,048

131

131 9 1,179

131

131 10 1,310

131

average

revenue

Total

revenue from the

sale of a product

divided by the

quantity of the

product sold.

The total revenue for each sales level is found by multiplying price by the corre-

sponding quantity the firm can sell. (Column 1 multiplied by column 2 in Table 9-2

yields column 3.) In this case, total revenue increases by a constant amount, $131,

for each additional unit of sales. Each unit sold adds exactly its constant price to

total revenue.

When a firm is pondering a change in its output, it will consider how its total rev-

enue will change as a result. What will be the additional revenue from selling

another unit of output? Marginal revenue is the change in total revenue, that is,

the extra revenue, that results from selling one more unit of output. In column 3,

Table 9-2, total revenue is zero when zero units are sold. The first unit of output

sold increases total revenue from zero to $131; marginal revenue for that unit is

$131. The second unit sold increases total revenue from $131 to $262, and marginal

revenue is again $131. Note in column 4 that, as is price, marginal revenue is a

constant $131. In pure competition, marginal revenue and price are equal. (Key

Question 3)

Graphical Portrayal

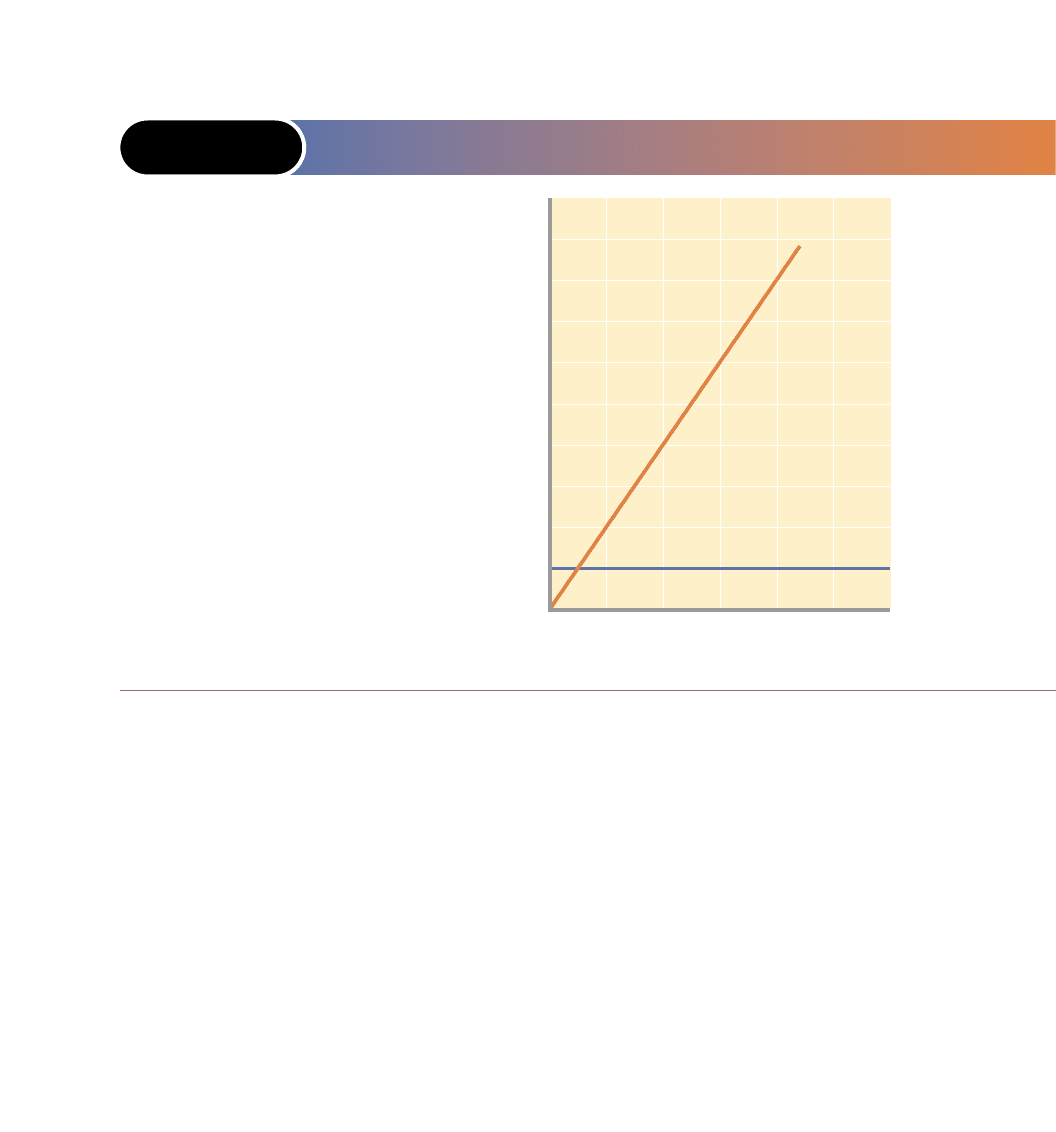

Figure 9-1 shows the purely competitive firm’s demand curve and total-revenue and

marginal-revenue curves. The demand curve (D) is horizontal, indicating perfect

price elasticity. The marginal-revenue curve (MR) coincides with the demand curve,

because the product price (and hence MR) is constant. Total revenue (TR) is a

straight line that slopes upward to the right. Its slope is constant because each extra

unit of sales increases TR by $131.

chapter nine • pure competition 217

total

revenue

The

total number of dol-

lars received by a

firm from the sale

of a product.

marginal

revenue

The

change in total rev-

enue that results

from selling one

more unit of a firm’s

product.

FIGURE 9-1 DEMAND, MARGINAL REVENUE, AND TOTAL

REVENUE OF A PURELY COMPETITIVE FIRM

TR

D

= MR

$1,179

1,048

917

786

655

524

393

262

131

0 24681012

Quantity demanded (sold)

Price and revenue

A purely competitive

firm can sell addi-

tional units of output

at the market price,

and thus its marginal-

revenue curve (MR)

coincides with its

perfectly elastic

demand curve (D).

The firm’s total-

revenue curve (TR)

is a straight upward-

sloping line.

Since the purely competitive firm is a price-taker, it can maximize its economic profit

(or minimize its loss) only by adjusting its output. In the short run, the firm has a

fixed plant. Thus, it can adjust its output only through changes in the amount of

variable resources (materials, labour) it uses. It adjusts its variable resources to

achieve the output level that maximizes its profit.

There are two ways to determine the level of output at which a competitive firm

will realize maximum profit or the minimum amount of loss. One method is to com-

pare total revenue and total cost; the other is to compare marginal revenue and mar-

ginal cost. Both approaches apply to all firms, whether they are pure competitors,

pure monopolists, monopolistic competitors, or oligopolists.

1

Total-Revenue–Total-Cost Approach: Profit-Maximization Case

With the market price of its product given by the market, the competitive producer

will ask: (1) Should we produce this product? (2) If so, in what amount? (3) What

economic profit (or loss) will we realize?

Let’s demonstrate how a firm in pure competition answers these questions, given

certain cost data and a specific market price. Our cost data are already familiar to

you because they are the fixed-cost, variable-cost, and total-cost data in Table 8-2,

repeated in columns 1 to 4 in Table 9-3. (Recall that these data reflect explicit and

implicit costs, including a normal profit.) Assuming that the market price is $131,

the total revenue for each output level is found by multiplying output (total prod-

uct) by price. Total revenue data are in column 5. Then in column 6 we find the profit

or loss at each output level by subtracting total cost, TC (column 4), from total rev-

enue, TR (column 5).

Should the firm produce? Definitely. It can realize a profit by doing so. How

much should it produce? Nine units. Column 6 tells us that this is the output at

which total economic profit is at a maximum. What economic profit (or loss) will the

firm realize? A $299 economic profit—the difference between total revenue ($1,179)

and total cost ($880).

Figure 9-2(a) compares total revenue and total cost graphically for this profit-

maximizing case. Observe again that the total revenue curve for a purely competitive

218 Part Two • Microeconomics of Product Markets

● In a purely competitive industry a large number

of firms produce a standardized product and no

significant barriers to entry exist.

● The demand of a competitive firm is perfectly

elastic—horizontal on a graph—at the market

price.

● Marginal revenue and average revenue for a

competitive firm coincide with the firm’s de-

mand curve; total revenue rises by the product

price for each additional unit sold.

Profit-Maximization in the Short Run

1

To make sure you understand these two approaches, we will apply them both to output deter-

mination under pure competition, but since we want to emphasize the marginal approach, we will

limit our graphical application of the total-revenue approach to a situation where the firm maxi-

mizes profits. We will then use the marginal approach to examine three cases: profit maximiza-

tion, loss minimization, and shutdown.

firm is a straight line (Figure 9-2). Total cost increases with output in that more pro-

duction requires more resources, but the rate of increase in total cost varies with the

relative efficiency of the firm. Specifically, the cost data reflect Chapter 8’s law of

diminishing marginal returns. From zero to four units of output, total cost increases

at a decreasing rate as the firm uses its fixed resources more efficiently. With addi-

tional output, total cost begins to rise by ever-increasing amounts because of the

diminishing returns accompanying more intensive use of the plant.

Total revenue and total cost are equal where the two curves in Figure 9-2(a) inter-

sect (at roughly two units of output). Total revenue covers all costs (including a nor-

mal profit, which is included in the cost curve) but there is no economic profit. For

this reason economists call this output a break-even point: an output at which a

firm makes a normal profit but not an economic profit. If we extended the data

beyond 10 units of output, another break-even point would occur where total cost

would catch up with total revenue somewhere between 13 and 14 units of output

in Figure 9-2(a). Any output between the two break-even points identified in the fig-

ure will produce an economic profit. The firm achieves maximum profit, how-

ever, where the vertical distance between the total-revenue and total-cost curves is

greatest. For our particular data, this is at nine units of output, where maximum

profit is $299.

The profit-maximizing output is easier to see in Figure 9-2(b), where total eco-

nomic profit is graphed for each level of output. Where the total-revenue and total-

cost curves intersect in Figure 9-2(a), economic profit is zero, as shown by the

total-profit line in Figure 9-2(b). Where the vertical distance between TR and TC is

greatest in the upper graph, economic profit is at its peak ($299), as shown in the

lower graph. This firm will choose to produce nine units, since that output maxi-

mizes its profit.

chapter nine • pure competition 219

TABLE 9-3 THE PROFIT-MAXIMIZING OUTPUT FOR A PURELY

COMPETITIVE FIRM: TOTAL-REVENUE–TOTAL-COST

APPROACH (PRICE $131)

PRICE: $131

(1) (2) (3) (4) (5) (6)

Total Total Total Total Total Profit (+)

product fixed cost, variable cost, cost, revenue, or loss (–)

(output), Q TFC TVC TC TR

0 $100 $ 0 $ 100 $ 0 $–100

1 100 90 190 131 – 59

2 100 170 270 262 – 8

3 100 240 340 393 + 53

4 100 300 400 524 +124

5 100 370 470 655 +185

6 100 450 550 786 +236

7 100 540 640 917 +277

8 100 650 750 1,048 +298

9 100 780 880 1,179 +299

10 100 930 1,030 1,310 +280

break-even

point

An output

at which a firm

makes a normal

profit but not an

economic profit.