Baker K.R. Optimization Modeling with Spreadsheets

Подождите немного. Документ загружается.

Requirements per unit

STD DLX Hours available

Department 1 (hrs) 4 4 600

Department 2 (hrs) 3 2 400

Department 3 (hrs) 2 4 500

Profit per unit $50 $40

The Operations Manager at General Appliance would like to maximize profit contribution for

the month by choosing production quantities for the two models.

B

To formulate an optimization model for this scenario, let variables STD and DLX represent

the number of Standard and Deluxe models produced (and sold). If we represent the demand for

the Standard model by X, we can formulate the optimization problem for GAC as follows.

Maximize z ¼ 50 STD þ 30 DLX

subject to

4 STD þ 4 DLX 600

3 STD þ 2 DLX 400

2 STD þ 4 DLX 500

STD X

DLX 25

Thus, for any value of X, we can solve the optimization problem and determine the optimal pro-

duction quantities of STD and DLX.

In probability language, the possible demand scenarios are called states of nature

(or simply states), to indicate that the conditions are beyond our control. A probability

distribution lists the possible states and associates a probability with each state. (For

convenience, we’ll number th e states.) In our example, we might have some market

intelligence that leads us to adopt the following probability distribution.

State 1 2 3

Demand 80 104 160

Probability 0.2 0.5 0.3

Our optimization model takes three forms, depending on which state occurs. For state

1, the optimal output mix is 80 Standard models and 70 Deluxe models. For state 2, the

optimal output mix is 104 Standard models and 44 Deluxe models. Finally, for state 3,

the optimal output mix is 116.7 Standard models and 25 Deluxe models.

If we could learn the demand state in advance, we could determine the optimal

production quantity by solving the linear program with the appropriate demand

parameter. The crux of the problem, however, is that the production decision

must be determined before demand is known. Because we decide on production

396

Appendix 4 Stochastic Programming

before demand is resolved, there may be a di fference between the quantity pro-

duced and the quantity sold to retailers. (In the deterministic model, this difference

does not arise because feasible production quantities are sure to be sold.) The pro-

babilistic scenario forces us to consider what happens when production and sales

don’t match.

For the purposes of our example, suppose that GAC can sell its excess inventory

through a discount channel and earn a profit contribution of $15. Now, we must dis-

tinguish between the number of items produced and the number sold in each channel,

since those can differ when demand is stochastic. Thus, we introduce the variable SS1

to represent the number of Standard models sold to retailers in state 1 and SX1to

represent the number of excess Standard models (sold to the discounter) in state 1.

Then, our model requires two constraints.

SS1 80

STD SS1 SX1 ¼ 0

If production exceeds the demand of 80, then the first constraint limits retail sales to

demand, while the second constraint sets the excess equal to the difference between

production and retail sales. On the other hand, if demand exceeds production, then

the second constraint limits sales to production. (The excess quantity will then be

zero, because retail sales are more profitable than discount sales.) We do not need

to track the excess Deluxe models because all units of the Deluxe will be sold.

A similar set of constraint pairs is required for the other states.

State 2

SS2 104

STD SS2 SX2 ¼ 0

State 3

SS3 160

STD SS3 SX3 ¼ 0

Finally, we must account for the profits in a consistent manner, recognizing that

sales levels depend on which state occurs. For state 1, the objective function can be

expressed as follows.

Z1 ¼ 50SS1 þ 15SX1 þ 30DLX

Rearranging terms

50SS1 þ 15SX1 þ 30DLX Z1 ¼ 0

We next add this equality constraint to the model, as a means of defin ing Z1 internally.

For the other two states, we insert similar equalities.

50SS2 þ

15SX2 þ 30DLX Z2 ¼ 0

50SS3 þ 15SX3 þ 30DLX Z3 ¼ 0

A4.1. One-Stage Decisions with Uncertainty 397

Guided by the theory of decision making under uncertainty, our objective is to

maximize the expected value of profit. Having accounted separately for the profit in

each state, we can compute this expected value as a probability-weighted average,

using the following formula.

z ¼ 0:2Z1 þ 0:5Z2 þ 0:3Z3

This expression is linear, as are all of the additional constraints, so when we include

them in our model, we still have a linear programming problem. The full spreadsheet

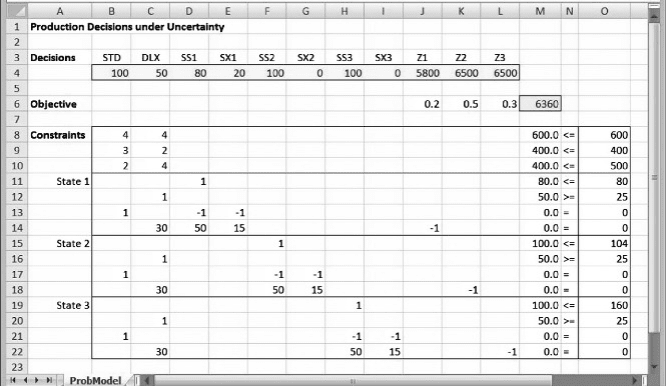

model is displayed in Figure A4.1. The constraints have been organized into four sets.

The first set of (three) constraints carries over from the original model and includes the

production decisions, which must be determined before the uncertainty about demand

gets resolved. The next set of four constraints corresponds to state 1, th e following set

of four constraints corresponds to state 2 and the final set of four constraints corre-

sponds to state 3. The expected value of profit appears in the objective function.

Recall that the original deterministic model contained five constraints and

two variables. This new model contains 15 constraints and 11 variables, somewhat

more than in the original model. But these values depend directly on the number of

outcomes in our probability model. Had we represented demand with ten outcomes

instead of three, the model would contain 43 constraints and 25 variables.

Although we can reduce the problem size slightly by substituting for the

profit variables Z1, Z2, and Z3, the model is more transparent if the profit measure

is tracked separately for each state and then simply weighted in the objective function

to show the expected value calculation clearly. This is one of our design principles for

stochastic programming models.

Figure A4.1. Stochastic program for Example A4.1.

398 Appendix 4 Stochastic Programming

A second principle is to modularize the linear programming formulation by gath-

ering together the constraints that correspond to a given state. In our example, that

meant appending three constraint modules to the basic production-hours constraints.

Because the problem is stochastic, targets that might be met in one state may lead

to surplus or shortage in another state, so we must introduce additional variables to

track the consequences.

Finally, a third principle illustrated by our example spreadsheet is that the initial

decision variables reappear in each of the modules. In particular, the production

decision variables STD and DLX occur in the relevant demand constraints within

each of the three modules.

The optimal solution to the model, which achieves an expected profit of $6360, is

displayed in Figure A4.1. The optimal production mix is 100 Standard models and 50

Deluxe models, which corresponds to none of the output mixes produced by the model

for the individual scenarios.

The production of 100 Standard models and 50 Deluxe models represents a policy

that recognizes the risks due to uncertain demand. Under state 1, we have excess

Standard models and must accept the lower profit in the discount channel for some

of our output. On the other hand, under state 3, and to some extent under state 2,

we have a shortage of Standard models and must accept the lower profit from selling

Deluxe models instead. It would be feasible to produce a larger number of Deluxe

models, and those additional models would be certain to sell. But the profit available

from this strategy would not offset the expected loss es that would occur from pro-

ducing fewer Standard models because of limited resources. The need to balance

the risks arises because we have only one decision period. A two-period scenario is

discussed next.

A4.2. TWO-STAGE DECISIONS WITH UNCERTAINTY

In the one-stage model, a decision is made, and then the uncertain state is revealed.

At that point, all conditions are determined, and the economic consequences can be

computed. A more general structure is a two-stage model, which contains some oppor-

tunity to react to the uncertainty. The technical term for this structure is stochastic

programming with recourse. Again, we illustrate the principles with a modification

of Example A4.2.

EXAMPLE A4.2

General Appliance Company (continued)

Although monthly demand at GAC is uncertain, the uncertainty is resolved about half

way through the month. At that point, it is still possible to alter production plans slightly. In par-

ticular, GAC can reschedule during the last week of the month, enough to raise the available

hours in each department by 12 percent. Now, the Operations Manager faces a decision invol-

ving possible rescheduling as well as determining the output mix. B

A4.2. Two-Stage Decisions with Uncertainty

399

The addition to monthly capacity can be implemented after the demand state has been resolved.

Thus, 72 additional hours can be brought on line in department 1, 48 additional hours in depart-

ment 2, and 56 more in department 3. (The production capability might come, for example, from

an opportunity to schedule some unplanned overtime or simply by reassigning personnel.) How

does this new opportunity affect the decision?

As before, an initial production decision must be made before the demand state is

known. Should the level of demand be higher than expected, however, there is still an

opportunity to produce additional items, perhaps to fill the gap between the initial pro-

duction and the newly determined demand, or else to take advantage of the additional

capacity. In this second round of production decisions no uncertainty exists, and we

can proceed as if we were in a deterministic environment.

The analysis builds on the previous example. One new feature is an additional set

of production decisions corresponding to the second-stage. Thus, we define STD1 and

DLX1 as the Standa rd and Deluxe production quantities made with the additional

hours in the case of state 1. Similarly, STD2 and DLX2 represent the additional pro-

duction quantities for state 2, and STD3 and DLX3 represent the additional production

quantities for state 3.

Suppose that state 1 occurs after initial production decisions have been made. The

second-stage decision problem calls for choosing STD1 and DLX1 subject to three

resource constraints and the need to track any surplus that might occur. The module

of resource constraints takes the following form.

4 STD1 þ 4 DLX1 72

3 STD1 þ 2 DLX1 48

2 STD1 þ 4 DLX1 56

Next, with the second-stage production variables defined, we can modify the

definitional constraints of the one-stage example and add the following equations

for the state 1.

STD þ STD1 SX1 SS1 ¼ 0

SS1 80

DLX þ DLX1 25

Similar constraints apply to the other states.

State 2

STD þ STD2 SX2 SS2 ¼ 0

SS2 104

DLX þ

DLX2 25

State 3

STD þ STD3 SX3 SS3 ¼ 0

SS3 160

DLX þ DLX3 25

400

Appendix 4 Stochastic Programming

Finally, as in the previous example, we can capture the profits in auxiliary

variables.

50SS1 þ 15SX1 þ 30DLX þ 30DLX1 Z1 ¼ 0

50SS2 þ 15SX2 þ 30DLX þ 30DLX2 Z2 ¼ 0

50SS3 þ 15SX3 þ 30DLX þ 30DLX3 Z3 ¼ 0

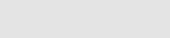

The entire model is shown in the spreadsheet of Figure A4.2. Here, again, the

model contains four modules, three of which correspond to the three demand states.

However, these are larger modules than in the one-stage example because of the

second production opportunity. For the two-stage model, we have 24 constraints

and 17 decision variables. Again, the model’s size depends on the number of states;

with ten states, our model would have 73 constraints and 45 decision variables.

Before we discuss the solution to the problem, we reiterate the three design

features shown in Figure A4.2.

†

A constraint module corresponds to each state.

†

The first-stage decisions appear in each of the modules corresponding to states.

†

Separate accounting is done for each of the objective function components that

correspond to states.

†

The objective function components are weighted by probabilities to construct

the overall expected value for the objective.

The solution displayed in Figure A4.2 has a complicated but logical pattern. The

initial production quantities are 98 Standard models and 52 Deluxe models. If state 1

occurs, the number of Standard models is already larger than demand, so additional

capacity will be devoted exclusively to 15 Deluxe models, bringing the total output

levels to 98 and 67. If state 2 occurs, the additional capacity will be used to bring

the number of Standard models up to retail demand and to add to the number of

Deluxe models, bringing the total output levels to 104 and 64. If state 3 occurs,

the additional capacity will be devoted exclusively to Standard models to the extent

available hours permit, bringing the totals to 114 and 52.

Thus, the initial production quantities leave several options open, and the optimal

plan takes one of three directions depending on the demand state. The expected profit

under the optimal plan is about $6994. By comparison , suppose we were to expand

the model in Figure A4.1 to reflect the full 112 percent capacity levels. The optimal

solution to that model (which has no recourse structure) achieves an expected profit

of only $6,952. Therefore, the ability to tailor our second-stage reactions to the sto-

chastic outcome allows us to achieve the greater profit level.

For another comparison, imagine that we could learn the demand state first and

then respond with a single production plan that had access to the incremental

12 percent capacity. For that situation, the expected profit (based on probabilities of

0.2, 0.5, and 0.3 for the three states, respectively) turns out to be $7103. It would

always be preferable to resolve uncertainty before making a production decision,

A4.2. Two-Stage Decisions with Uncertainty 401

but in this case, there is sufficient flexibility in the two-stage structure that the expected

profit is only about $109 lower for having to make the major decisions without know-

ing demand for sure. This low figure depends, of course, on the parameters of the

example, but it does suggest that the two-stage structure affords considerable flexi-

bility. Stochastic programming enables us to quantify this kind of flexibility.

A4.3. USING SOLVER

As described in Section A4.2, the optimization model for stochastic programming

with recourse can be viewed as an expanded linear program, with explicit treatment

of each random state. The expanded linear program can be developed and optimized

by running Solver. But keep in mind that our example contained essentially just five

constraints and two variables, only one of which was subject to uncertainty. Moreover,

that uncertainty was expressed in the form of a discrete probability distribution with

just three outcomes. For that small problem, the stochastic program was 24 by 17.

Stochastic programming models can become quite large, and constructing them can

be tedious and error-prone. We might wonder whether some of the modeling task

can be automated.

Risk Solver Platform has specialized capabilities for solving stochastic programs,

but to describe those capabilities, we must first examine its representation of probabil-

istic outcomes. RSP is an integrated software tool that uses probability distributions in

simulation models. A design feature in RSP is that only one simulation model can be

supported in a given workbook. Therefore, in building a stochastic programming

Figure A4.2. Stochastic program with recourse for Example A4.2.

402 Appendix 4 Stochastic Programming

model, or any simulation model, we should make sure that if our workbook contains

other worksheets, they do not contain probability distributions. (By contrast, RSP

supports one optimization model per worksheet.)

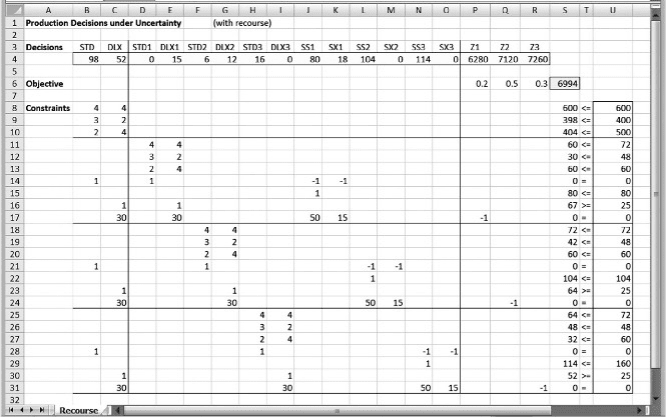

Suppose, for example, that we wish to construct a cell that behaves like demand

for Standard models in Exa mple A4.1. The relevant type of distribution in Solver is the

Discrete distribution, which we can access from the RSP ribbon via the Simulation

Model group of commands. Choose a cell to contain the demand model and select

Distributions

Q Custom Q Discrete. The Discrete distribution window offers the oppor-

tunity to specify values and weights, which are equivalent to outcomes and relative

probabilities. For our example of demand for Standard refrigerators, the values

would be {80, 104, 160} and the weights would be {0.2, 0.5, 0.3}. Entering these

values produces th e display shown in Figure A4.3.

By specifying the probability distribution for demand, we allow Solver to draw

samples from this distribution for the purposes of simulation. In general, a simulation

sample may not necessarily represent the relative probabilities in a distribution faith-

fully. In our example, if we draw 10 samples, we expect to obtain the value 80 about a

fifth of the time, which means twice. But in Monte Carlo sampling, we may draw the

Figure A4.3. Discrete distribution in risk solver platform.

A4.3. Using Solver 403

value 80 just once, or perhaps three times. Only in a large sample can we depend on

drawing the value 80 about 20 percent of the time. However, we can make the out-

comes conform much more closely to the given distribution by invoking Latin

Hypercube sampling. (This option can be selected by from the drop-down menu for

Options: select All Options and then select the Latin Hypercube radio button under

Sampling Method. In the same window, select All Trials as the Value to Display,

and set Trials per Simulation equal to 10.) Under Latin Hypercube sampling, a

sample of ten draws from the distribution will contain 80 twice, 104 five times, and

160 three times, conforming precisely to the frequencies in the given probability

model.

Because Solver has the capability of representing discrete probability models as

simulated outcomes, the stochastic program can be represented efficiently on a spread-

sheet. The recourse variables need only be represented once in the model. The spread-

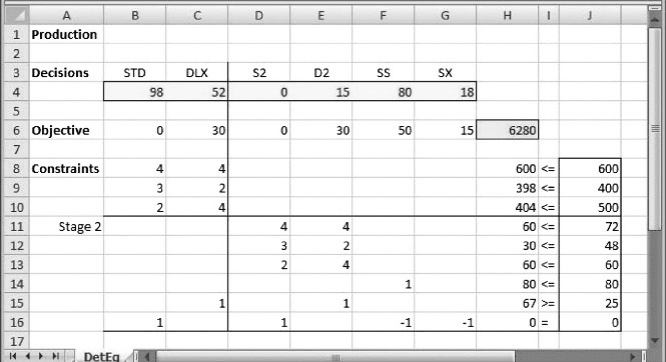

sheet model for Example A4.2 is shown in Figure A4.4.

In the spreadsheet model, the original variables are STD and DLX, as before. The

second stage decision variables are S2 and D2, representing the quantities produced

using the 12 percent resource capability at the second stage, and SS and SX,as

before, represent the number of Standard models sold to retailers and the number of

excess Standard m odels (sold to discounters). These last four decision variables are

designated Recourse variables in specifying the model elements in the task pane. In

addition, the demand di stribution is imbedded in cell J14.

The worksheet has only one explicit representation of the second stage, but Solver

can sample (10 times) for the value in cell J14, following the probability distribution.

1

Thus, Solver actually solves the problem two times with the demand outcome of 80 in

Figure A4.4. Solver model for the stochastic program of Example A4.2.

1

To obtain the optimal solution, we must set the Stochastic Transformation option on the Platform tab of

the task pane either to Deterministic Equivalent or to Automatic.

404 Appendix 4 Stochastic Programming

cell J14, five times with 104, and three times with 160. The corresponding optimal sol-

utions are stored and can be retrieved by clicking on the arrows in the Tools group on

the ribbon. When the number showing between the arrows is 1, the optimal solution

corresponding to the first simulation sample is displayed. When the number showing

is 2, the second sample is displayed, and so on. By clicking through the 10 outcomes,

we can verify that three sets of decisions appear, according to the demand outcome.

These sets of decisions, taken from row 4 of the worksheet, are summarized in the

table below.

Demand STD DLX S2 D2 SS SX

80 98 52 0 15 80 18

104 98 52 6 12 104 0

160 98 52 16 0 114 0

These results match those in Figure A4.2. However, the table layout makes it clearer

that the first-stage production quantities are 98 Standard models and 52 Deluxe

models, but the second-stage quantities depend on the demand outcome.

Finally, the expected-value objective function is not explicit in the worksheet for

Solver. However, to find the optimal value of the objective function, we can go to the

drop-down menu between the two arrows in the Tools group and select Sample Mean.

In place of the simulation trial number, the letter

m

appears. In addition the objective

function cell and the decision variable cells also display averages over the sample

outcomes. In the case of the objective function, the mean value corresponds to the

optimal value of the transformed model, in this case, $6994.

Stochastic programming can be a powerful form of analysis. It allows us to

address issues of uncertainty instead of making deterministic simp lifications. And

in the case of stochastic programming models with recourse, the solution helps us

tailor our responses to uncertain outcomes. However, there is a modeling cost for

this capability. Whereas a deterministic description allows us to meet targets exactly,

it is not possible to be as specific in a probabilistic setting. Instead, we may have to

invent variables to measure the surplus and shortage outcomes that occur when uncer-

tain factors are present. These new variables become part of a more complicated view

of the problem than we captured in the original, deterministic model. In addition, we

have to come up with a reasonable probability model for the uncertain elements of the

problem. In our example, we illustrated the use of a simple discrete distribution with

only three outcomes. In many cases, three outcomes might not be sufficient to provide

a meaningful description of the uncertainty. However, as we add outcomes to the

probability model, we expand the size of the model by requiring additional sets of

variables and constraints. Thus, accommodating even one source of uncertainty can

lead to an order of magnitude expansion in the size of the model. Modeling multiple

sources compounds this complexity. For these reasons, stochastic programming

models are still not widely used, but now that Solver can provide solutions, that situ-

ation may change.

A4.3. Using Solver 405