Masters G.M. Renewable and Efficient Electric Power Systems

Подождите немного. Документ загружается.

288 ECONOMICS OF DISTRIBUTED RESOURCES

3.75

3

2.25

1.5

0.75

0

Week

Hour

24

1

Marginal cost ($/kWh)

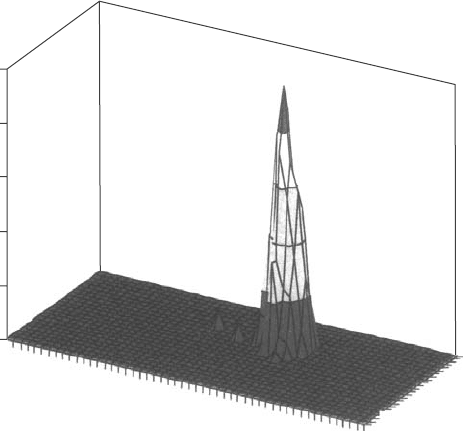

Figure 5.27 Area-and-time (ATS) studies can identify feeders where distributed gener-

ation and demand-side management programs can be particularly cost effective. This is a

particular PG&E feeder in the early 1990s. From Swisher and Orans (1996).

V = iR, and there is power loss due to i

2

R heating of the wires. The longer

the distance and the greater the current, the more there will be voltage drop and

power loss in the wires. If, however, a distributed generation source provides

some of its own power, or if loads can be reduced through customer efficiency,

the current and power that the grid needs to supply will drop and so will grid

losses. Moreover, if the DG source actually delivers power to the grid, line losses

will be reduced even more.

Injecting power onto the grid not only provides voltage support to offset iR

drops and reduce i

2

R losses, it can also raise the power factor of the lines. Recall

that when voltage and current are out of phase with each other, more current must

be provided to deliver the same amount of true power (watts) capable of doing

work. Improving the power factor is usually accomplished by adding banks of

capacitors to the line, but it can also be helped if DG systems are designed to

inject appropriately phased reactive power. Improved power factor reduces line

current, which reduces voltage sag and line losses. On top of that, a better power

factor also helps distribution transformers waste less energy, supply more power,

and extend their lifetime.

5.7.4 Reliability Benefits

Most power outages are caused by faults in the transmission and distribution

system—wind and lightning, vehicular accidents, animals shorting out the

DISTRIBUTED BENEFITS 289

wires—not generation failures. To the extent that a customer can provide some

fraction of their own power during those outages, especially to critical loads such

as computers and other digital equipment, the value of the added reliability can

easily surpass the cost of generation by orders of magnitude. Such emergency

standby power is now often provided with back-up generators, but such systems

are usually not designed to be operated continuously, nor are they permitted

to do so given their propensity to pollute. This means that they don’t provide

any energy payback under normal circumstances. Battery systems and other

uninterruptible power supplies (UPS) can’t cover sustained outages on their own

without additional backup generators, so they have the same disadvantages of

not being able to help pay for themselves by routinely delivering kilowatt-hours.

Fuel cells, on the other hand, can operate in parallel with the grid. With

natural gas reformers, or sufficient stored hydrogen, they can cover extended

power outages. With no emissions or noise they be housed within a building

and can be permitted to run continuously so they are an investment with annual

returns in addition to providing protection against utility outages.

5.7.5 Emissions Benefits

As concerns about climate change grow, there is increasing attention to the role

of carbon emissions from power plants. The shift from large, coal-fired power

plants to smaller, more efficient gas turbines and combined-cycle plants fueled

by natural gas can greatly reduce those emissions. Reductions result from both

the increased efficiency that many of these plants have and the lower carbon

intensity (kgC/GJ) of natural gas. As Table 5.11 indicates, natural gas emits only

about half the carbon per unit of energy when it is burned as does coal.

Calculating the reduction in emissions in conventional power plants that would

be gained by fuel switching from coal to gas is straightforward. To do so for

cogeneration is less well defined. One approach to calculating carbon emissions

from CHP plants is to use the energy chargeable-to-power (ECP) measure. Recall

that ECP subtracts the displaced boiler fuel no longer needed from the total input

energy, which, in essence, attributes all of the fuel (and carbon) savings to the

electric power output. The following example illustrates this approach.

TABLE 5.11 Carbon Intensity of Fossil Fuels Based on High-Heating Values

(HHV)

a

Energy Density

(kJ/kg)

Carbon Content

(%)

Carbon Intensity

(kgC/GJ)

Anthracite coal 34,900 92 26.4

Bituminous coal 27,330 75 27.4

Crude oil 42,100 80 19.0

Natural gas 55,240 77 13.9

a

HHV includes latent heat in exhaust water vapor.

Source: IPCC (1996) and Culp (1979).

290 ECONOMICS OF DISTRIBUTED RESOURCES

Example 5.18 Carbon Emission Reductions with CHP. Use the ECP method

to determine the reduction in carbon emissions associated with a natural-gas-fired,

combined-cycle CHP having 41% electrical efficiency and 44% thermal effi-

ciency. Assume that the thermal output would have come from an 83% efficient

boiler. Compare it to that of a 33.3% efficient conventional bituminous-coal-fired

power plant.

Solution. The energy chargeable to power is given by (5.39)

ECP =

Total thermal input − Displaced thermal input

Electrical output

=

3600

η

P

1 −

η

H

η

B

kJ/kWh

ECP =

3600

0.41

1 −

0.44

0.83

= 4126 kJ/kWh

Using the 13.9-kgC/GJ carbon intensity of natural gas provided in Table 5.11 gives

Carbon chargeable to power =

4126 kJ/kWh × 13.9 kgC/GJ

10

6

kJ/GJ

= 0.0573 kgC/kWh

The coal plant has no displaced thermal input, so its ECP is the full

ECP =

3600

0.333

= 10,811 kJ/kWh

Using 27.4 kgC/GJ as its carbon intensity from Table 5.11, we obtain

Carbon chargeable to power =

10,811 kJ/kWh × 27.4 kgC/GJ

10

6

kJ/GJ

= 0.296 kgC/kWh

The efficient CHP combined-cycle plant reduces carbon emissions by 81%.

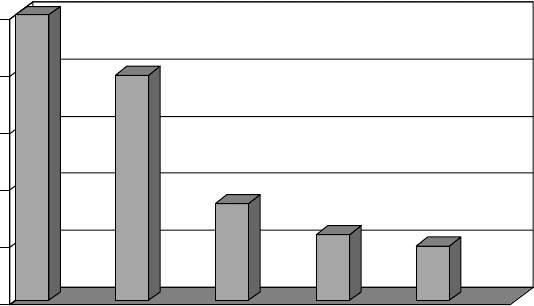

Application of the above method for evaluating carbon emissions to a number of

power plants results in the bar chart shown in Fig. 5.28. The bar heights represent

emissions compared to those from the 33.3%-efficient coal plant just evaluated.

INTEGRATED RESOURCE PLANNING (IRP) AND DEMAND-SIDE MANAGEMENT (DSM) 291

0

20

40

60

80

100

Relative Carbon Emissions (%)

100

AVERAGE

COAL

33%Eff

BEST

COAL

42%Eff

N. GAS

COMB-CYCLE

49% Eff

N. GAS, CHP

SIMPLE-CYCLE

30% Elect Eff

49% Thermal Eff

N. GAS, CHP

COMB-CYCLE

41% Elect Eff

44% Thermal Eff

79

34

23

19

Figure 5.28 Relative carbon emissions for various power plants compared to the average

coal plant. CHP units assume thermal output replaces an 83% efficient gas boiler.

5.8 INTEGRATED RESOURCE PLANNING (IRP) AND DEMAND-SIDE

MANAGEMENT (DSM)

In the 1980s, regulators began to recognize that energy conservation could be

treated as a “source” of energy that could be directly compared with traditional

supply sources. If utilities could help customers be more efficient in their use of

electricity, delivering the same energy service with fewer kilowatt-hours, and if

they could do so at lower cost than supplying energy, then it would be in the

public’s interest to encourage that to occur. What emerged is a process called

integrated resource planning (IRP) or, as it is sometimes referred to, least-cost

planning (LCP).

The new and defining element of IRP was the incorporation of utility pro-

grams that were designed to control energy consumption on the customer’s side

of the electric meter. These are known as demand-side management (DSM) pro-

grams. While DSM most often refers to programs designed to save energy, it has

been defined in a broader sense to refer to any program that attempts to modify

customer energy use. As such it includes:

1. Conservation/energy efficiency programs that have the effect of reducing

consumption during most or all hours of customer demand.

2. Load management programs that have the effect of reducing peak demand

or shifting electric demand from the hours of peak demand to non-peak-

time periods.

292 ECONOMICS OF DISTRIBUTED RESOURCES

3. Fuel substitution programs that influence a customer’s choice between elec-

tric or natural gas service from utilities. For example, the electricity needed

for air conditioning can be virtually eliminated by replacing a compressive

refrigeration system with one based on absorption cooling.

DSM programs have included a wide range of strategies, such as (1) energy

information programs, including energy audits; (2) rebates on energy-efficient

appliances and other devices; (3) incentives to help energy service companies

(ESCOs) reduce commercial and industrial customer demand for their clients;

(4) load control programs to remotely control customer appliances such as water

heaters and air conditioners; (5) tariffs designed to shift or reduce loads (time-

of-use rates, demand charges, real-time pricing, interruptible rates).

5.8.1 Disincentives Caused by Traditional Rate-Making

Electric utilities have traditionally made their money by selling kilowatts of power

and kilowatt-hours of energy, so the question arises as to how they could possibly

find it in their best interests to sell less, rather than more, electricity. To understand

that challenge, we need to explore the role of state-run public utility commissions

(PUCs) in determining the rates and profits that investor-owned utilities (IOUs)

have traditionally been allowed to earn.

A fairly common rate-making process is based on utilities providing evidence

for costs, and expected demand, to their PUC in what is usually referred to as a

general rate case (GRC). General rate cases often focus only on the non-fuel com-

ponent of utility costs (depreciation of equipment, taxes, non-fuel operation and

maintenance costs, return on investment, and general administrative expenses).

Dividing these revenue requirements by expected energy sales results in a base-

case ratepayer cost per kWh. Fuel costs, which may change more rapidly than

the usual schedule of general rate case hearings, may be treated in separate pro-

ceedings. In general, changes in fuel costs are simply passed on to the ratepayers

as a separate charge in their bills.

To understand how this process encourages sales of kWh and discourages

DSM, consider the simple graph of revenue requirements versus expected energy

sales shown in Fig. 5.29. In this example, the utility has a fixed annual revenue

requirement of $300 million needed to recover capital costs of equipment along

with other fixed costs, plus an additional amount that depends on how many

kilowatt-hours are generated. In this example, each additional kilowatt-hour of

electricity generated costs an additional amount of one cent. This 1¢/kWh is

called the short-run marginal cost, which means that it is based on operating

existing capacity longer. There is also long-run marginal cost, which applies

when the additional power needed triggers an expansion of the existing power

plants, transmission lines, or distribution system.

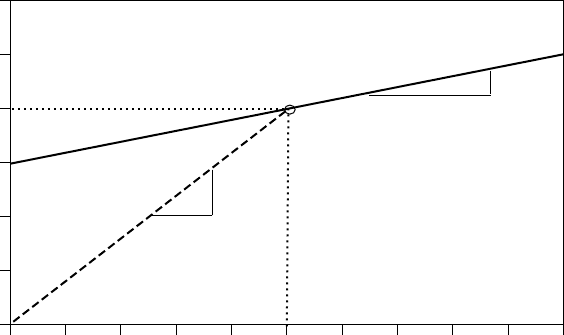

If the utility in Fig. 5.29 projects that it will sell 10 billion kWh/yr, then annual

revenues of $400 million would be needed. The ratio of the two is an average

base rate of 4¢/kWh, which is what the utility would be allowed to charge until

the next general rate case is heard.

INTEGRATED RESOURCE PLANNING (IRP) AND DEMAND-SIDE MANAGEMENT (DSM) 293

20181614121086420

0

100

200

300

400

500

600

Estimated Sales (Billion kWh/yr)

Revenue Required (Million $/yr)

Average cost

4 ¢/kWh

Marginal cost

1 ¢/kWh

Figure 5.29 Estimated sales of 10 billion kWh would require $400 million in revenue,

so the (non-fuel) base rate would be 4¢/kWh.

Consider now the perverse incentives that would encourage this utility to sell

more kWh than the 10 billion estimated in Fig. 5.29. Having established a price of

4¢/kWh, any sales beyond the estimated 10 billion kWh/yr would yield revenues

of 4¢ for each extra kWh sold. Since each extra kWh generated has a marginal

cost of only 1¢, and it is being sold at 4¢, there will be a net 3¢ profit for each

extra kWh that can be sold.

Notice, too, that the example utility loses money if it sells less than 10 billion

kWh. Generating one fewer kWh reduces costs by 1¢, but reduces revenue by 4¢.

In other words, this rather standard practice of rate-making not only encourages

utilities to want to sell more energy, it also strongly discourages conservation

that would reduce those sales.

5.8.2 Necessary Conditions for Successful DSM Programs

As the above example illustrates, traditional rate-making has tended to reward

energy sales and penalize energy conservation, no matter what the relative costs

of supply-side and demand-side options might be. During the 1980s and early

1990s, energy planners and utility commissions grappled with the problem of

finding fair and equitable rate-making procedures that would reverse these ten-

dencies, allowing cost-effective energy-efficiency to compete. Three conditions

were found to be necessary for DSM to be successful:

1. Decoupling utility sales from utility profits.

2. Recovery of DSM program costs to allow utilities to earn profits on DSM.

3. DSM incentives to encourage utilities to prefer DSM over generation.

294 ECONOMICS OF DISTRIBUTED RESOURCES

While there are several approaches that regulators have taken to decouple

utility profits from sales, the electric rate adjustment mechanism (ERAM) is a

good example of one that works quite effectively. ERAM simply incorporates any

revenue collected, above or below 1 year’s forecasted amount, into the following

year’s authorized base-rate revenue, thereby eliminating incentives to sell more

kWh and removing disincentives to reduce kWh sales. Clearly, decoupling is a

necessary condition for DSM to work, but it is not sufficient.

The second condition allows utilities to earn profits on demand-side programs

just as they do on supply-side investments. Recovery of DSM program costs

can be accomplished by including them in the rate base alongside capital costs

of power plants and other utility infrastructure. In this way, supply-side and

demand-side investments would both earn whatever rate of return the regulators

would allow. Alternatively, DSM costs might be included as an expense that is

simply passed along to the ratepayer.

Experience has shown that just decoupling sales and profits, along with rate-

basing or expensing DSM costs, does not provide sufficient encouragement for

utilities to actively pursue customer energy efficiency. Additional incentives for

the utilities and their stockholders seems to be needed. Shared savings programs

have emerged in which shareholders are allowed to keep some fraction of the net

savings that DSM programs provide. The following example illustrates this idea.

Example 5.19 A Shared-Savings Program. Suppose that a utility offers a $2

rebate on 18-W, 10,000-h, compact fluorescent lamps (CFLs) that produce as

much light as the 75-W incandescents they are intended to replace. Suppose

that it costs the utility an additional $1 per CFL to administer the program. The

utility has a marginal cost of electricity of 3¢/kWh, and 1 million customers are

expected to take advantage of the rebate program.

If a shared savings program allocates 15% of the net utility savings to share-

holders and 85% to ratepayers, what would be the DSM benefit to each?

Solution

Energy savings = (75 − 18) W/CFL × 10 kh × $0.03/kWh × 10

6

CFL

= $17.1 million

Program cost = ($2 + $1)/CFL × 10

6

CFL = $3 million

Net savings to utility = $17.1 million − $3 million = $14.1 million

Shareholder benefit = 15% ×$14.1 million = $2.12 million

Ratepayer savings = 85% ×$14.1 million = $11.99 million

INTEGRATED RESOURCE PLANNING (IRP) AND DEMAND-SIDE MANAGEMENT (DSM) 295

In the above example, it was quite easy to calculate the energy savings asso-

ciated with replacing 75-W incandescents with 18-W CFLs, assuming that their

rated 10,000-h lifetime is realized. For many other efficiency measures, how-

ever, the savings are less easy to calculate with such confidence. Exactly how

much energy will be saved by upgrading the insulation in someone’s home, for

example, is not at all easy to predict.

Further complicating load reduction estimates are the problems of free rid-

ers and take-backs. Free riders are customers who would have purchased their

energy efficiency devices even if the utility did not offer an incentive. In the

above example, it was assumed that all 1 million rebates went to customers

who would not have purchased CFLs without them. Take-backs refer to cus-

tomers who change their behavior after installing energy-efficiency devices. For

example, after insulating a home a user may be tempted to turn up the thermostat,

thereby negating some fraction of the energy savings.

While free riders, take-backs, and uncertainties in estimating energy savings

may result in less DSM value to the utility than anticipated, one can argue that

these are more than offset by the environmental advantages of not generating

unneeded electricity. Some utilities have, in fact, tried to incorporate environ-

mental externalities into the avoided cost benefits of DSM.

5.8.3 Cost Effectiveness Measures of DSM

The goal of integrated resource planning is to minimize the cost to customers of

reliable energy services by suitably incorporating supply-side and demand-side

resources. A proper measure of cost-effectiveness on the demand side, unfortu-

nately, is largely in the eyes of the beholder; that is, the most cost-effective DSM

strategy for stockholders may be different from the best strategy as seen by util-

ity customers. In fact, utility customers can also see things differently depending

on whether the customer is someone who takes advantage of the conservation

incentives, or whether it is a customer who either cannot, or will not, take advan-

tage of the benefit (e.g., they already purchased the most efficient refrigerator on

their own before an incentive was offered). To account for such differences of

perspective, a number of standardized DSM cost-effectiveness measures have

been devised.

The evaluation of DSM cost-effectiveness measures is complicated by such

factors as what type of DSM it is (e.g. appliance efficiency, commercial peak-

power reduction, fuel switching) and what assumptions are appropriate to deter-

mine future costs and savings. The following descriptions are vastly simplified

for clarity; for greater detail, see, for example, CPUC (1987).

Ratepayer Impact Measure (RIM) Test. The RIM test is primarily a measure

of what happens to utility rates as a result of the DSM program. For a DSM

program to be cost effective using the RIM test, utility rates must not increase.

296 ECONOMICS OF DISTRIBUTED RESOURCES

(a)

(b)

Revenue required

kWh sales

Revenue required

kWh sales

Figure 5.30 Marginal cost can be higher than average cost when the cost curve is

nonlinear. (a) Smoothly increasing costs. (b) Jumps caused by capacity expansion.

That is, even nonparticipants must not see an increase in their electric bills (or at

least a lower increase than they would have seen without DSM), which is why

this is sometimes referred to as the no-losers test. Clearly, this is a difficult test to

pass. For example, any reduction in demand for the utility modeled in Fig. 5.29

will result in an increase in the average cost of electricity. But, this example

utility has a simple, linear relationship between demand and price, which may

not always be the case. Increasing demand may mean that less efficient, more

expensive power plants get used more often (Fig. 5.30a) or it may trigger the

need for new generation, transmission, and distribution capacity (Fig. 5.30b).

Avoiding or delaying new capacity expansions is often a major driver motivating

DSM programs.

A necessary condition for a measure to pass the RIM test is that the marginal

cost of electricity (including fuel costs) must be greater than the average cost.

Moreover, the only way to keep rates from increasing is to have the DSM program

cost less than the difference between the marginal cost of electricity and the

average cost. For example, if the average cost of a kWh of electricity is 5¢ and

the marginal cost is 6¢, then a DSM program has to cost less than 1¢ to save a

kWhtopasstheRIMtest.

Example 5.20 The RIM Test for a CFL Program. Suppose that the util-

ity offering the CFL rebate program in Example 5.18 has an average cost of

electricity of 2¢/kWh. Will the program pass the RIM test?

Solution. Since the marginal cost of electricity (3¢/kWh) is more than the aver-

age cost (2¢/kWh), the DSM program might pass the RIM test. To check,

however, we need to find the per kWh cost of the CFL program. With a $2 rebate

and a $1 administrative cost, DSM costs $3 per CFL so the cost of conserved

energy is

DSM cost =

$3/CFL

(75 − 18)W/CFL × 10 kh

= $0.0052/kWh = 0.52¢/kWh

INTEGRATED RESOURCE PLANNING (IRP) AND DEMAND-SIDE MANAGEMENT (DSM) 297

To pass the RIM test, the DSM cost must be less than the difference between the

marginal and average cost to the utility:

Marginal cost − Average cost = 3¢/kWh − 2¢/kWh

= 1¢/kWh > 0.52 ¢/kWh

So the RIM test is satisfied and electric rates will decrease with this program.

Total Resource Cost (TRC) Test. The TRC test asks whether society as a

whole is better off with DSM. It is again a cost–benefit calculation in which

benefits result from reduced costs of fuel, operation, maintenance, and trans-

mission losses, as well as potential reduction in needed power plant capacity,

as before. Total costs are somewhat different since they not only include DSM

administrative costs incurred by the utility, but also add any extra cost the cus-

tomer pays when purchasing the more efficient product. Since the utility pays the

rebate and the customer collects it, the net impact of the rebate itself on societal

cost is zero, so it is simply not included in the TRC test on either side of the

benefit–cost calculation. For measures passing the TRC test, utility rates may

go up or down, but average utility bills will decrease. Nonparticipants may see

an increase in their bills. The TRC test is the most commonly used measure of

DSM cost effectiveness.

Example 5.21 The TRC Test for a CFL Program. Suppose 75-W incan-

descents costing $0.50 each have an expected lifetime of 1000 h. The utility is

offering a $2 rebate to encourage customers to replace those with 10,000-h, 18-W

CFLs that normally cost $7. The utility has a marginal cost of $0.03/kWh. It will

cost the utility $1 per CFL to administer the program. Does this measure satisfy

the TRC test?

Solution. Since the TRC test excludes the cost of the rebate, the utility cost per

CFL is just $1 per CFL.

Ignoring the rebate, the customer spends $7 for a 10,000-h CFL. To obtain

the same light would require purchasing ten 1000-h incandescents at 50¢ each,

for a total of $5. The extra cost to the consumer is therefore $7 − $5 = $2 for

each CFL.

Total cost to society of the conservation measure (regardless of the amount

of rebate) is the sum of the utility cost and consumer cost, or $1 + $2 = $3 for

each CFL.

The avoided cost benefit seen by the utility is

Avoided cost benefit = (75 − 18) W × 10 kh × $0.03/kWh

= $17.10 per CFL